Bermuda swaptions occupy a unique position in the interest rate derivatives landscape. They combine elements of both European and American-style exercise features, offering structured flexibility while maintaining cost efficiency. For institutional investors, asset-liability managers, and structured products desks, understanding Bermuda swaptions is essential for effective interest rate risk management.

This comprehensive guide explains how Bermuda swaptions function, how they differ from other swaption styles, and why their valuation often requires advanced quantitative methods such as Monte Carlo simulation.

What Is a Bermuda Swaption?

A Bermuda swaption is an over-the-counter (OTC) derivative contract that grants the holder the right—but not the obligation—to enter into an interest rate swap on one of several predetermined exercise dates.

Unlike a European swaption, which can be exercised only at maturity, or an American swaption, which can be exercised at any time prior to expiration, a Bermuda swaption allows exercise on multiple specific dates defined at inception.

In practice, these exercise dates are often scheduled periodically (e.g., quarterly or semiannually) and align with swap payment dates.

Bermuda swaptions are primarily used by:

- Banks and financial institutions

- Pension funds

- Insurance companies

- Corporate treasury departments

- Structured note issuers

They serve as tools for managing duration exposure and reshaping fixed-versus-floating rate obligations.

How Bermuda Swaptions Work in Interest Rate Markets

To understand Bermuda swaptions, it is important to first understand the underlying instrument: the interest rate swap.

An interest rate swap is a contractual agreement between two counterparties to exchange streams of interest payments—typically fixed-rate payments for floating-rate payments. Only the net cash flow difference is exchanged; principal amounts are not transferred.

A swaption is an option granting the right to enter into such a swap.

There are two primary types:

- Payer Swaption – Right to pay fixed and receive floating

- Receiver Swaption – Right to receive fixed and pay floating

A Bermuda swaption allows the holder to initiate the swap on one of several specified dates rather than on a single date or continuously.

Example Scenario

Consider a corporation that anticipates issuing debt in stages over the next three years. Instead of locking in an interest rate immediately, it purchases a Bermuda payer swaption that can be exercised annually. If interest rates rise significantly at any of those exercise points, the firm can enter into a fixed-for-floating swap to hedge exposure.

This staggered optionality creates flexibility while controlling premium costs.

Comparing Bermuda, American, and European Swaptions

The defining characteristic of these instruments lies in their exercise style. Each structure has distinct pricing implications and risk characteristics.

European Swaptions

- Exercise allowed only at maturity

- Simplest structure

- Lowest premium (all else equal)

- Valuation often uses closed-form models

American Swaptions

- Exercise allowed at any time prior to expiration

- Maximum flexibility

- Highest premium

- More complex valuation

Bermuda Swaptions

- Exercise allowed on multiple predetermined dates

- Hybrid structure

- Moderate premium

- Complex valuation due to discrete early-exercise opportunities

The naming convention follows geographic analogy: Bermuda sits between Europe and America, just as the exercise flexibility sits between European and American option styles. A related instrument, sometimes referred to as a “Canary swaption,” allows even fewer exercise opportunities than Bermuda style.

From a structuring perspective, Bermuda swaptions provide counterparties the ability to customize exercise schedules according to funding or hedging needs.

Why Bermuda Swaptions Are Structurally Attractive

Bermuda swaptions offer several strategic advantages in institutional portfolios:

1. Controlled Flexibility

The holder gains multiple decision points without paying the full premium required for continuous exercise rights.

2. Lower Cost Than American Style

Because exercise is restricted to specific dates, the probability of optimal exercise is reduced relative to American options. This lowers the option’s time value and therefore its premium.

3. Better Fit for Liability Management

Exercise dates can align with:

- Bond call dates

- Loan repricing schedules

- Structured product reset dates

- Pension liability adjustments

4. Risk-Adjusted Hedging

They enable dynamic interest rate exposure adjustments in environments characterized by yield curve volatility.

However, flexibility introduces modeling complexity.

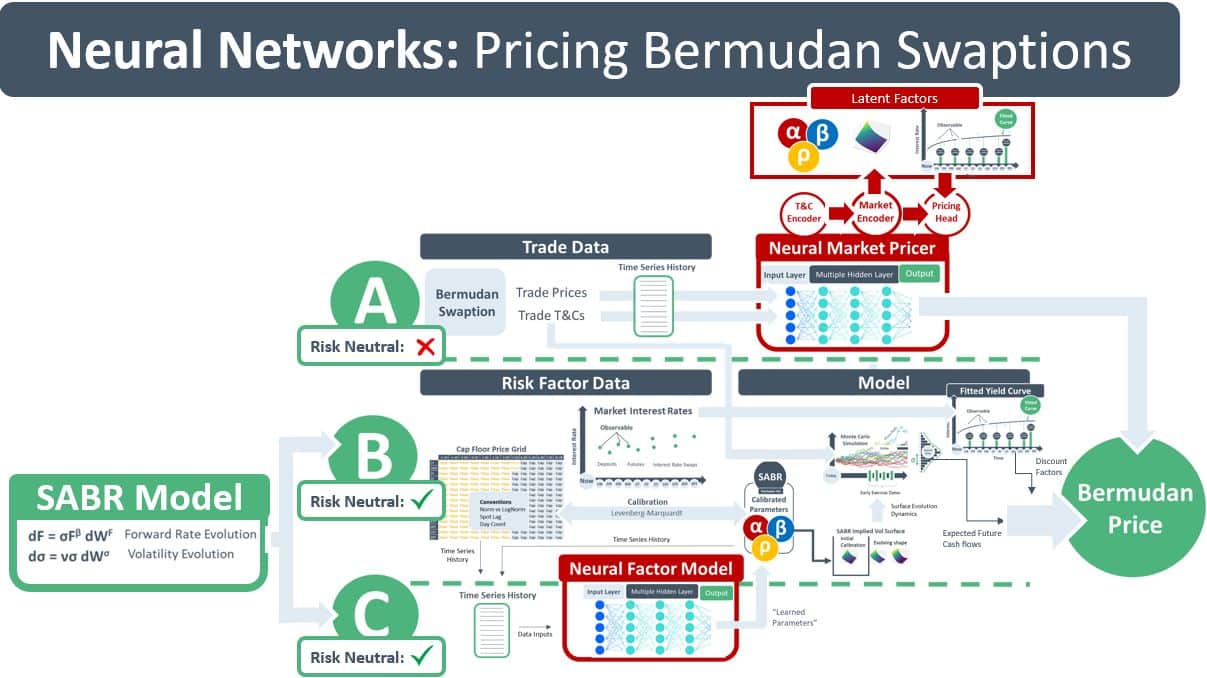

Pricing Bermuda Swaptions: Why It’s More Complex

Pricing Bermuda swaptions is significantly more challenging than pricing European swaptions.

European swaptions can often be valued using analytical models such as Black’s model for interest rate options. These models rely on closed-form solutions under specific volatility and distribution assumptions.

Bermuda swaptions, however, incorporate multiple early-exercise opportunities. At each exercise date, the holder must evaluate whether immediate exercise yields greater value than continuation.

This creates a dynamic optimization problem.

The Role of Monte Carlo Simulation

Because of the multiple potential exercise dates and path dependency of interest rates, Monte Carlo simulation is frequently used for valuation.

Monte Carlo methods simulate thousands (or millions) of potential future interest rate paths under a risk-neutral framework. At each potential exercise date, the model estimates:

- The immediate exercise value

- The expected continuation value

The option is exercised at points where intrinsic value exceeds continuation value.

One widely used approach is the Least Squares Monte Carlo (LSMC) method, originally developed for American-style options. It is also applicable to Bermuda swaptions due to their discrete exercise schedule.

Monte Carlo pricing captures:

- Volatility term structure

- Correlation dynamics

- Yield curve movements

- Mean reversion behavior

Because of computational intensity, these models are typically implemented in institutional risk systems rather than retail platforms.

Cost Comparison: Why Bermuda Swaptions Are Cheaper Than American Swaptions

Option premiums reflect flexibility.

American swaptions command the highest premiums because holders can exercise at any point before expiration. This maximizes optionality and increases the likelihood of exercising at optimal rates.

Bermuda swaptions restrict exercise to specific dates, reducing the probability of optimal timing. As a result:

- Premiums are lower than American-style swaptions

- Premiums are higher than European-style swaptions

This middle-ground pricing makes Bermuda swaptions attractive for institutions seeking optionality without excessive cost.

Risk Considerations and Market Applications

Bermuda swaptions are widely used in:

- Callable bond hedging

- Structured note issuance

- Mortgage-backed securities risk management

- Asset-liability management (ALM)

For example, callable bonds effectively embed Bermuda-style options. The issuer can call the bond on specific dates, mirroring Bermuda exercise features.

From a risk management standpoint, valuation depends on:

- Forward rate volatility

- Yield curve shape

- Time to maturity

- Exercise frequency

- Counterparty credit risk

Since Bermuda swaptions trade OTC, contracts are negotiated bilaterally. This introduces credit exposure and collateral considerations under ISDA agreements.

When Should Investors Use Bermuda Swaptions?

Bermuda swaptions are particularly suitable when:

- Interest rate direction is uncertain

- Exercise flexibility is desired but continuous flexibility is unnecessary

- Hedging dates are known in advance

- Budget constraints limit American swaption premiums

They are less suitable when continuous optionality is critical or when liquidity constraints favor simpler European instruments.

For institutional desks, selection depends on:

- Risk tolerance

- Hedge horizon

- Volatility expectations

- Capital efficiency requirements

Final Thoughts

Bermuda swaptions represent a sophisticated hybrid instrument within the broader interest rate derivatives market. By offering multiple predetermined exercise dates, they strike a balance between cost efficiency and flexibility.

Their valuation requires advanced quantitative modeling—most commonly Monte Carlo simulation—because of embedded early-exercise decision points. While more complex than European swaptions, they remain less expensive than American alternatives.

For institutional investors managing rate exposure, callable liabilities, or structured products, Bermuda swaptions provide a strategic tool that aligns financial flexibility with premium discipline.

Understanding their mechanics, pricing dynamics, and risk implications is essential for anyone operating in modern fixed-income and derivatives markets.